Contractor Stack · Part 11

Estimating and Proposal Software

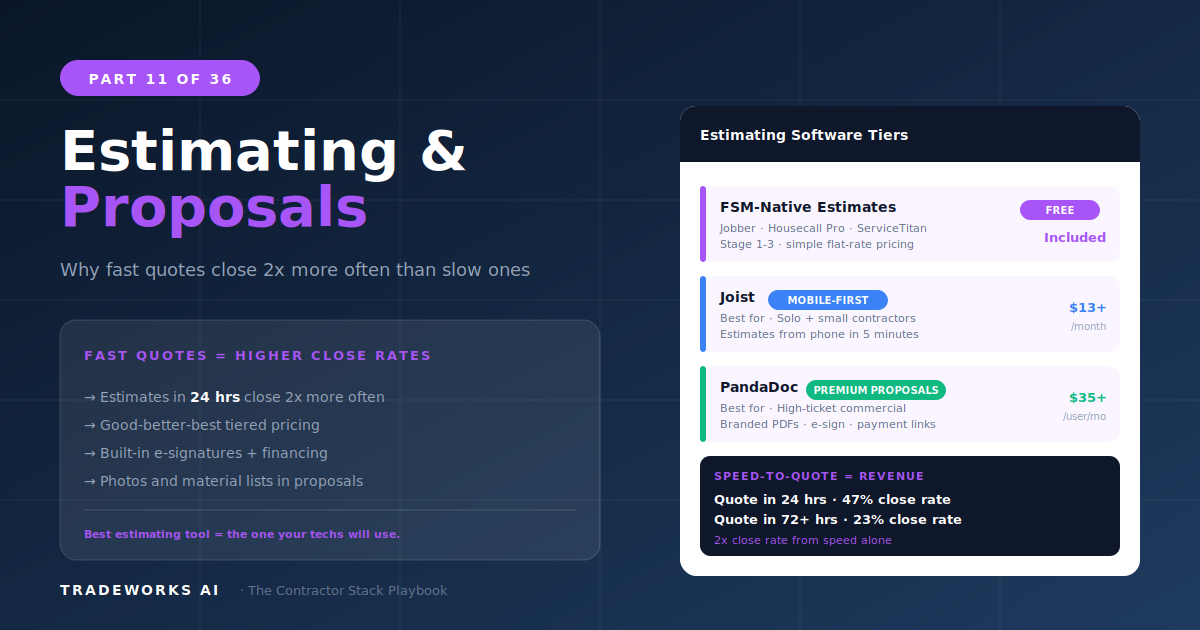

The best estimating software for contractors depends on trade and proposal complexity. For HVAC, plumbing, and electrical contractors usi...

The best payment processing solution for most contractors is the one built into their FSM platform. Housecall Pro, Jobber, ServiceTitan, and most field service management tools include integrated payment processing at 2.5 to 3.5 percent plus a per-transaction fee. The integration advantage is decisive: when a technician completes a job, the customer receives a one-click payment link on their phone, the payment is recorded in the FSM and synced to accounting automatically, and the contractor gets paid in 1 to 3 business days. For contractors processing over $1 million annually, every 0.5 percentage point in processing fees represents $5,000 in annual cost — making fee comparison and ACH alternatives worth serious evaluation.

Speed to payment follows the same principle as speed to estimate and speed to lead: the faster the transaction happens after the service is complete, the higher the collection rate. A customer who receives a one-click payment link via text message while the technician is still in the driveway pays within minutes. A customer who receives a paper invoice in the mail pays in 30 to 45 days — if they pay at all.

Digital payment through FSM-integrated processing reduces average collection time from 30 to 45 days to 1 to 3 days. For a contractor processing $100,000 per month, the cash flow improvement from collecting in 3 days versus 30 days is equivalent to a $90,000 interest-free loan that you no longer need. The processing fee pays for itself in cash flow velocity alone.

Your FSM’s built-in payment processing is the default recommendation for one reason: zero integration friction. The job-to-invoice-to-payment workflow is a single unbroken chain. The technician marks the job complete, the customer receives a payment link, the payment is recorded in the FSM, and the FSM syncs to accounting. No manual entry. No reconciliation gaps. No third-party middleware.

Processing fees for FSM-native payments range from 2.5 to 3.5 percent plus $0.15 to $0.30 per transaction. This is slightly higher than standalone processors like Square (2.6% + $0.10) or PaySimple (2.49% + interchange). The question is whether the fee difference justifies the integration complexity of a separate processor.

For a contractor processing $50,000/month: the difference between 2.6% (Square) and 3.0% (FSM-native) is $200/month. That $200 buys integrated payment tracking, automatic reconciliation, and zero bookkeeper time spent matching payments to invoices. For most contractors, the integration value exceeds the fee savings.

Square is the standalone payment processor that most contractors encounter first. The free card reader, transparent flat-rate pricing (2.6% + $0.10 in person, 2.9% + $0.30 online), and simple setup make it the natural choice for Stage 1 contractors who do not yet have an FSM. Square’s POS system is also relevant for contractors with a showroom or counter sales operation.

Square’s limitation for contractors is the disconnect from FSM data. Square processes the payment, but the FSM does not automatically record it against the correct job, customer, and invoice. Manual reconciliation is required. For a contractor processing 20+ transactions per week, this reconciliation time negates the fee savings versus FSM-native processing.

Stripe is the developer’s payment processor. It powers online payments for websites, custom booking forms, and API-driven payment flows. If TradeWorks AI or another agency builds a custom payment page for a contractor’s website, Stripe is likely the backend processor. Most contractors never interact with Stripe directly — it runs behind the scenes of other platforms.

For contractors with custom website payment forms, Stripe’s 2.9% + $0.30 online rate is competitive. Stripe’s strength is programmability, not simplicity. If you need a payment processor you can configure without writing code, Square or your FSM’s native option is the better choice.

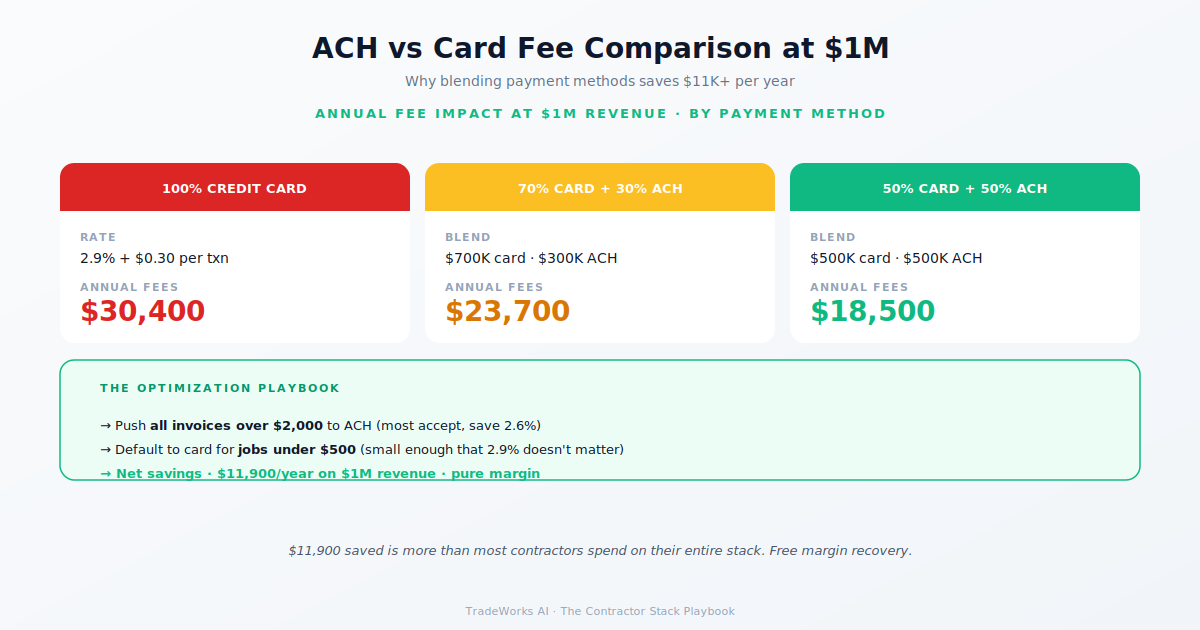

PaySimple targets contractors who process high volumes and want lower per-transaction rates through interchange-plus pricing. The platform also offers ACH (direct bank transfer) payments, which process at 0.5 to 1.0 percent with no per-transaction fee — dramatically lower than credit card rates.

ACH payments are the cost optimization lever for contractors processing large invoices. On a $5,000 HVAC installation, credit card processing at 3% costs $150. ACH at 0.75% costs $37.50. The savings compound: a contractor processing $500,000 annually through ACH instead of credit cards saves $11,250 per year in processing fees. The trade-off is customer convenience — ACH requires bank account details and takes 3 to 5 business days to settle versus 1 to 2 days for credit cards.

Processing fees feel small on individual transactions but compound significantly at annual scale:

$500,000 annual revenue at 2.6% (Square) = $13,000 in fees

$500,000 annual revenue at 3.0% (FSM-native) = $15,000 in fees

$500,000 annual revenue at 2.49% + interchange (PaySimple) = ~$12,450 in fees

$500,000 annual revenue at 0.75% ACH (large invoices only) = $3,750 in fees

The $2,000 annual difference between Square and FSM-native is real but must be weighed against bookkeeper reconciliation time (Part 6). The $9,000+ savings from ACH is substantial and worth offering as a payment option for invoices above $1,000.

Stage 1 (no FSM yet): Square. Simple, transparent, free hardware. Upgrade to FSM-native when you adopt an FSM.

Stage 2–5 (any contractor with FSM): FSM-native payments. The integration value exceeds the fee premium for most contractors. Supplement with ACH option for invoices over $1,000.

Stage 3–4 (high volume, fee-sensitive): PaySimple or negotiate FSM payment rates. Contractors processing $1M+ annually should negotiate processing fees with their FSM provider or evaluate standalone processors with interchange-plus pricing.

Large invoices ($2,000+): Offer ACH as a payment option alongside credit cards. The fee savings on large tickets are significant and many commercial customers prefer ACH for accounting reasons.

Yes. Credit card acceptance increases close rates because customers can authorize work immediately without writing a check or visiting an ATM. The 2.5 to 3.5 percent processing fee is a cost of doing business that is offset by faster payment collection, higher close rates, and reduced collections effort. Offer ACH as an alternative for large invoices to reduce fees on high-ticket transactions.

ACH (direct bank transfer) at 0.5 to 1.0 percent is the cheapest per-transaction option. For credit cards, interchange-plus pricing through PaySimple or negotiated FSM rates offer the lowest card processing fees. The cheapest overall approach: FSM-native payments for convenience on standard tickets, ACH option for invoices above $1,000 to $2,000.

FSM-native payments typically charge 2.5 to 3.5 percent plus $0.15 to $0.30 per transaction, compared to Square at 2.6 percent plus $0.10. The fee difference on a $500 job is approximately $2 to $5. The integration value of FSM-native payments — automatic job-to-payment reconciliation, no manual data entry, synchronized accounting — typically exceeds this fee difference unless processing volume is very high.

Most contractors are paying $400–900 per month for software they barely use, while losing thousands more in hidden costs from manual processes and missed callbacks. Our free audit grades your stack against the maturity model and identifies the highest-ROI changes you can make this quarter.

The best estimating software for contractors depends on trade and proposal complexity. For HVAC, plumbing, and electrical contractors usi...

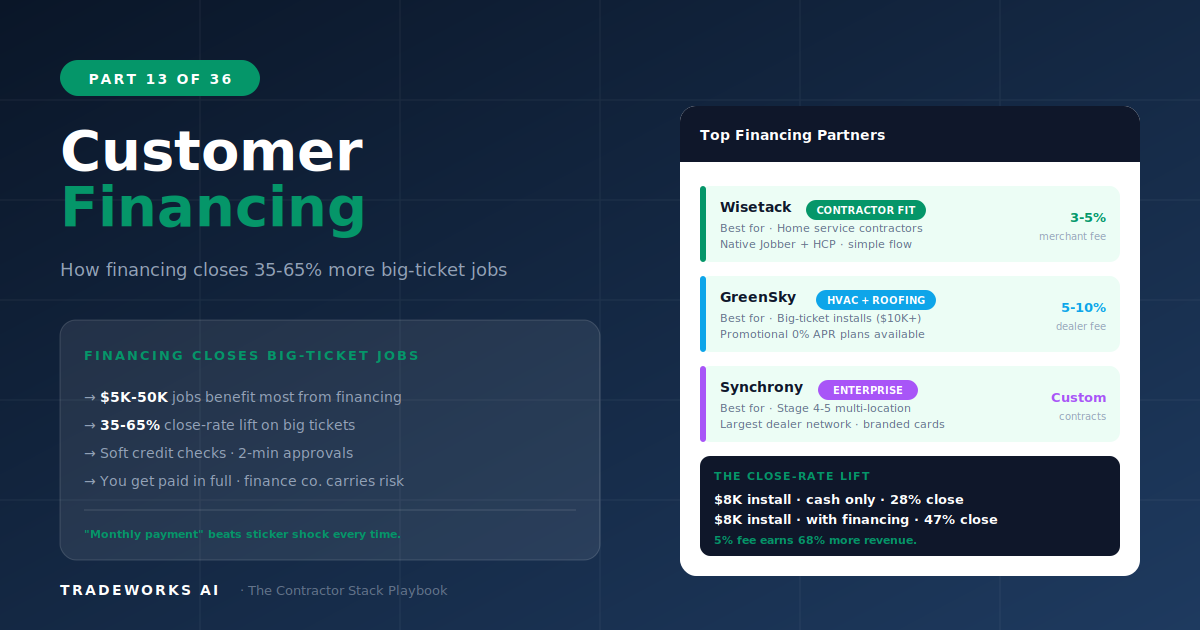

Customer financing for contractors increases average ticket size by 30 to 40 percent and close rates by 15 to 25 percent on projects abov...