Contractor Stack · Part 20

Inventory and Fleet Management

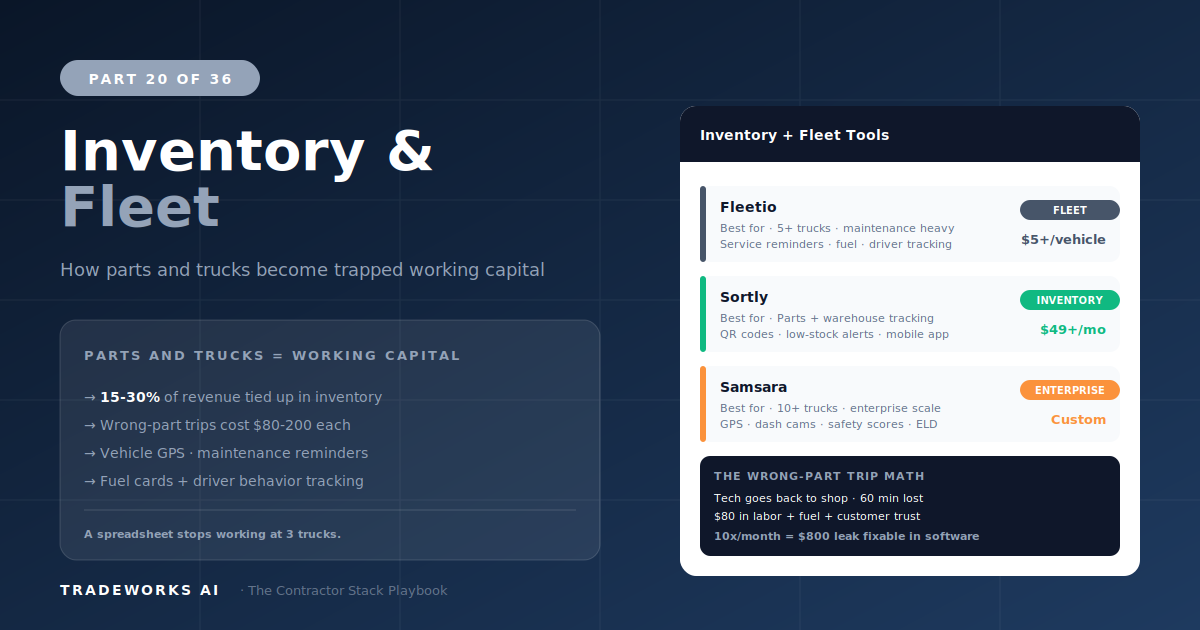

The best fleet management software for contractors is Fleetio ($5–$10 per vehicle per month) for maintenance scheduling, fuel tracking, a...

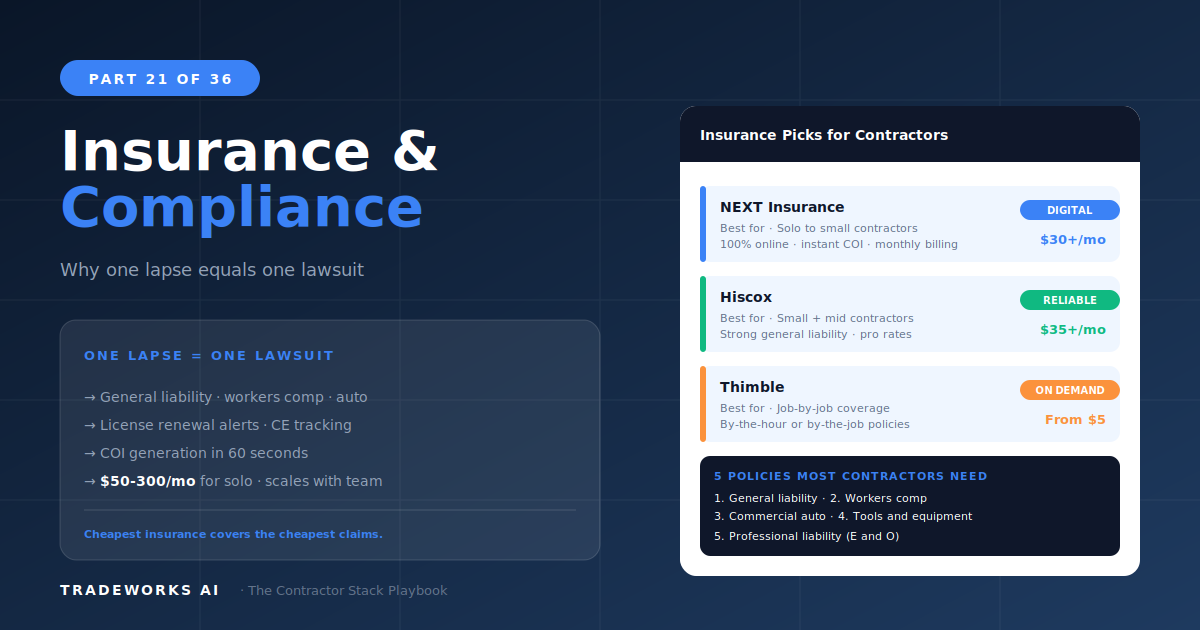

The best insurance platform for most contractors getting started or shopping for competitive rates is Next Insurance ($25–$300+ per month), which offers instant online quotes, digital certificates of insurance, and policy management through a modern app. For part-time or project-based contractors, Thimble ($5–$300+/month) provides on-demand coverage that can be activated per job. Licensing compliance is equally critical: an expired license can cost $5,000 to $50,000 or more in fines, lost contracts, and legal liability depending on the state and violation. Digital license tracking tools and calendar-based renewal reminders eliminate the most common compliance failure: forgetting to renew.

Insurance for contractors is not a nice-to-have. It is required by law in most states, required by general contractors on commercial projects, required by many homeowner associations, and increasingly verified by platforms like Angi, Thumbtack, and Google Local Services Ads before contractors can advertise. Operating without proper insurance is operating on borrowed time.

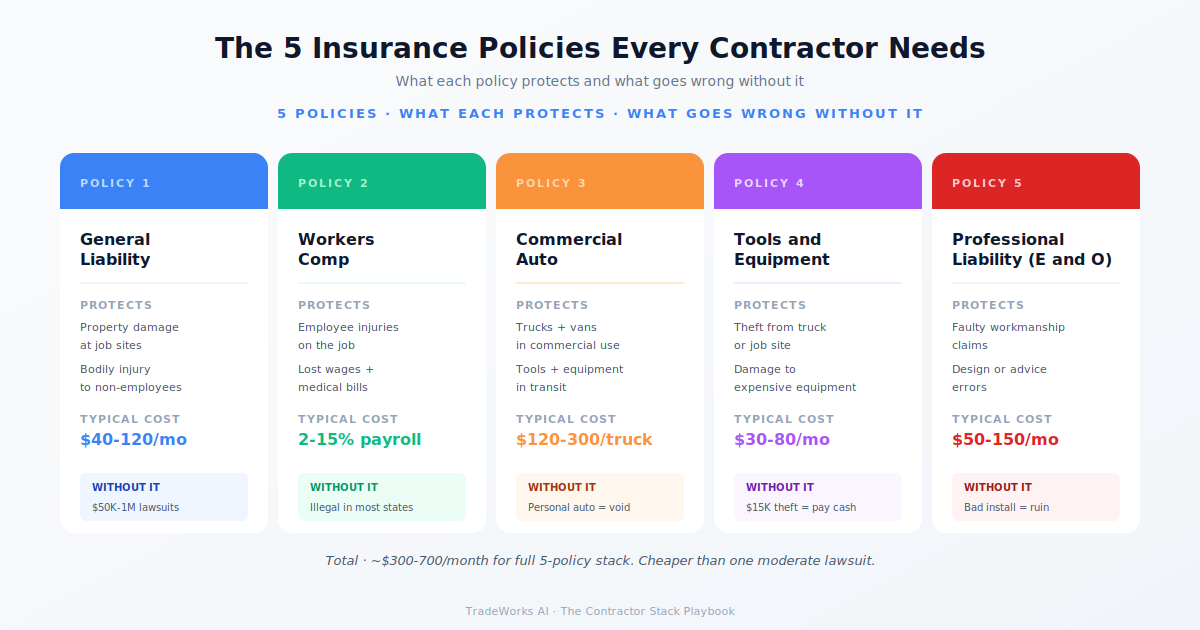

The four insurance types every contractor needs:

General Liability (GL): Covers damage to customer property and third-party injuries caused by your work. Required for virtually all contractor operations. Typical cost: $30 to $150/month for $1 million coverage depending on trade and revenue.

Workers’ Compensation: Covers employee injuries on the job. Required by law in most states once you have employees. Cost varies significantly by trade: HVAC and plumbing are lower risk than roofing and electrical. Typical range: $1 to $5 per $100 of payroll.

Commercial Auto: Covers vehicles used for business. Personal auto policies typically exclude business use — a claim filed while driving to a job site can be denied. Required for any vehicle used regularly for work.

Professional Liability / Errors & Omissions: Covers claims resulting from faulty workmanship, design errors, or professional negligence. Not required by law but strongly recommended for contractors performing work that carries long-term liability (electrical, plumbing, HVAC installations).

Next Insurance is the digital-first insurance platform built for small businesses and contractors. The entire process is online: quote in minutes, buy immediately, and receive a digital certificate of insurance (COI) that can be shared with general contractors and clients via email or link. Policy management, endorsements, and claims filing happen through the app or website.

Next Insurance’s advantage for contractors is speed and convenience. When a general contractor calls and says “I need your COI by end of day or you’re off the project,” Next delivers instantly. Traditional agents may take 24 to 48 hours. The coverage options include general liability, workers’ comp, commercial auto, and professional liability, with the ability to bundle for discounts.

The trade-off is personalization. Next Insurance is not going to build a custom risk management strategy for a $5 million multi-trade operation. For straightforward coverage needs at Stage 1–4, it is efficient and competitively priced. For complex operations, a traditional agent provides tailored coverage design.

8-Criteria Score: Trade Fit 4/5, Size 4/5, Integration 3/5, Mobile 5/5, Learning Curve 5/5, Pricing 4/5, Data Ownership 3/5, Support 3/5. Composite: 31/40.

Thimble offers on-demand insurance coverage that can be activated by the hour, day, week, or month. For part-time contractors, seasonal workers, or businesses that take on occasional specialty projects outside their normal scope, Thimble provides flexible coverage without year-long commitments. Need general liability for a weekend project? Activate coverage Friday, deactivate Monday.

The on-demand model is genuinely innovative but comes with limitations: coverage options are narrower than full-service platforms, per-day pricing is more expensive than annualized rates, and claims handling is limited to the coverage period. Thimble is ideal for Stage 1 contractors testing the waters, not for established businesses with continuous operations.

8-Criteria Score: Trade Fit 3/5, Size 2/5 (small/part-time), Integration 2/5, Mobile 5/5, Learning Curve 5/5, Pricing 3/5, Data Ownership 2/5, Support 2/5. Composite: 24/40.

CoverWallet operates as a multi-carrier marketplace: submit your information once and receive quotes from multiple insurance carriers. This comparison shopping approach can surface better rates than going directly to a single carrier, particularly for workers’ comp and commercial auto where rates vary significantly between carriers for the same risk profile.

Traditional insurance agents remain the best option for Stage 3–5 contractors with complex operations: multiple trades, large fleets, employee counts above 20, commercial project requirements, and claims history that requires specialized underwriting. A good agent also provides claims advocacy — when a claim is filed, the agent navigates the process on your behalf. Digital platforms handle routine coverage well but lack this personal advocacy layer.

An expired contractor license is one of the most expensive compliance failures in the industry. Consequences vary by state but typically include:

Fines ranging from $1,000 to $10,000+ per violation

Inability to pull permits, stopping all active projects

Void insurance coverage (some policies exclude unlicensed work)

Loss of eligibility for GC subcontracting, platform listings, and government work

Personal liability exposure for the business owner

The most common cause of license expiration is not negligence — it is forgetting. A license renewed every two years is easy to lose track of, especially when the business is focused on daily operations. Digital tracking eliminates this risk:

Calendar reminders: Set renewal alerts 90, 60, and 30 days before every license, insurance policy, and certification expiration. Use Google Calendar, your FSM’s task system, or a dedicated compliance tracker.

Document storage: Digitize all licenses, certificates, and policies in a cloud-accessible folder (Google Drive, Dropbox). Every team member who might need to produce a COI or license copy should have access.

Compliance dashboard: For Stage 3+ contractors with multiple licenses, certifications, and insurance policies, a spreadsheet or Notion database tracking every document with its expiration date, renewal requirements, and responsible person provides centralized visibility.

Use this checklist annually to verify all insurance and licensing is current:

General liability policy: active, adequate coverage limits, COI accessible digitally

Workers’ compensation: active, employee count updated, experience modifier reviewed

Commercial auto: all vehicles listed, coverage matches fleet size, new vehicles added

Contractor license: current, renewal date tracked, continuing education credits complete

Trade-specific certifications: EPA 608 (HVAC), backflow certification (plumbing), journeyman/master licenses

Business license: municipal and county business licenses renewed

Bond (if applicable): surety bond current and adequate for project requirements

Platform verifications: Google Local Services, Angi, Thumbtack insurance and license uploads current

Stage 1 (startup/part-time): Thimble for flexible on-demand coverage. Upgrade to Next Insurance when operations become continuous.

Stage 1–4 (straightforward coverage): Next Insurance. Digital-first, instant COIs, competitive rates, modern management. Primary recommendation for most contractors.

Stage 2–4 (rate shopping): CoverWallet for multi-carrier comparison, especially workers’ comp and commercial auto where rates vary significantly between carriers.

Stage 3–5 (complex operations): Traditional agent with contractor specialization. Justified when coverage design, claims advocacy, and risk management strategy exceed digital platform capability.

General liability for a small contractor typically costs $30 to $150 per month for $1 million in coverage. Workers’ comp costs $1 to $5 per $100 of payroll, varying significantly by trade (roofing is more expensive than cleaning). Commercial auto ranges from $100 to $300 per vehicle per month. Total insurance cost for a 5-person HVAC contractor: approximately $500 to $1,200 per month. Digital platforms like Next Insurance generally offer competitive rates for straightforward coverage needs.

No. Personal auto policies typically exclude regular business use. If you are involved in an accident while driving to or from a job site, a personal policy can deny the claim. Commercial auto insurance is required for any vehicle used regularly for business operations, including personal vehicles used for work commutes to job sites.

Consequences vary by state but commonly include fines ($1,000–$10,000+), inability to pull permits (stopping all active projects), voided insurance coverage for unlicensed work, and loss of platform listing eligibility. In some states, performing licensed work without a current license is a criminal offense. Set renewal reminders 90 days in advance to prevent expiration.

Recommended for any contractor performing work with long-term liability: HVAC installations with 10-year warranties, electrical work with fire risk, plumbing with water damage potential, and any design-build work. Professional liability covers claims that general liability does not: faulty workmanship, design errors, and professional negligence that causes damage after the project is complete.

Most contractors are paying $400–900 per month for software they barely use, while losing thousands more in hidden costs from manual processes and missed callbacks. Our free audit grades your stack against the maturity model and identifies the highest-ROI changes you can make this quarter.

The best fleet management software for contractors is Fleetio ($5–$10 per vehicle per month) for maintenance scheduling, fuel tracking, a...

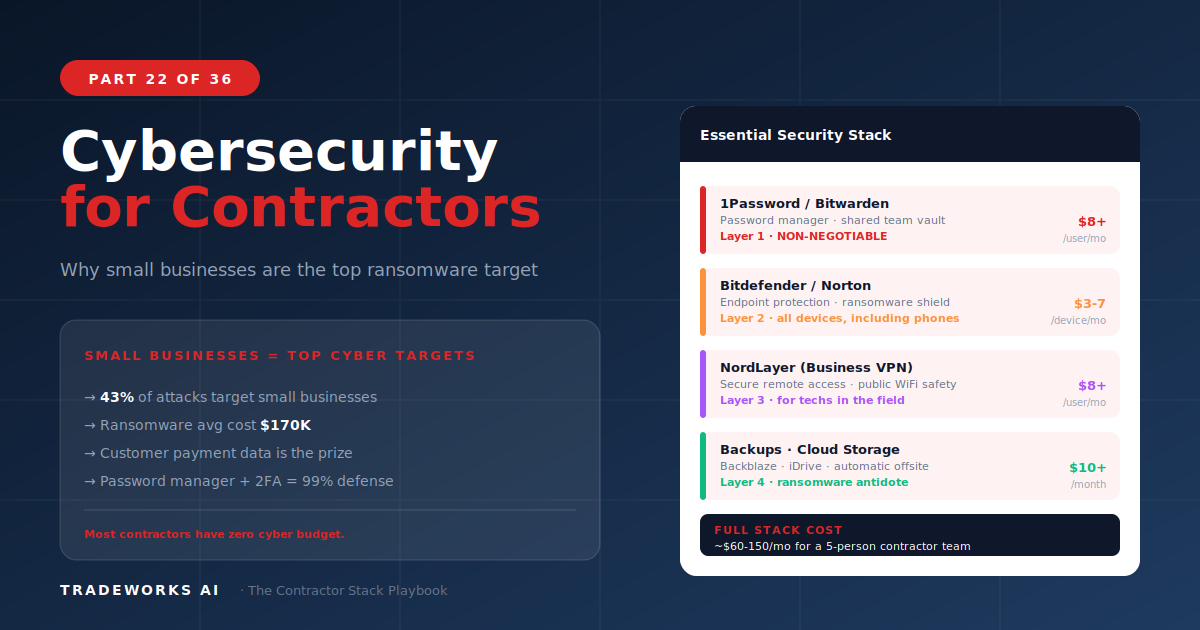

A complete cybersecurity stack for contractors costs approximately $50 per month and protects against threats that cost unprotected small...