Real Estate Tech · Part 12

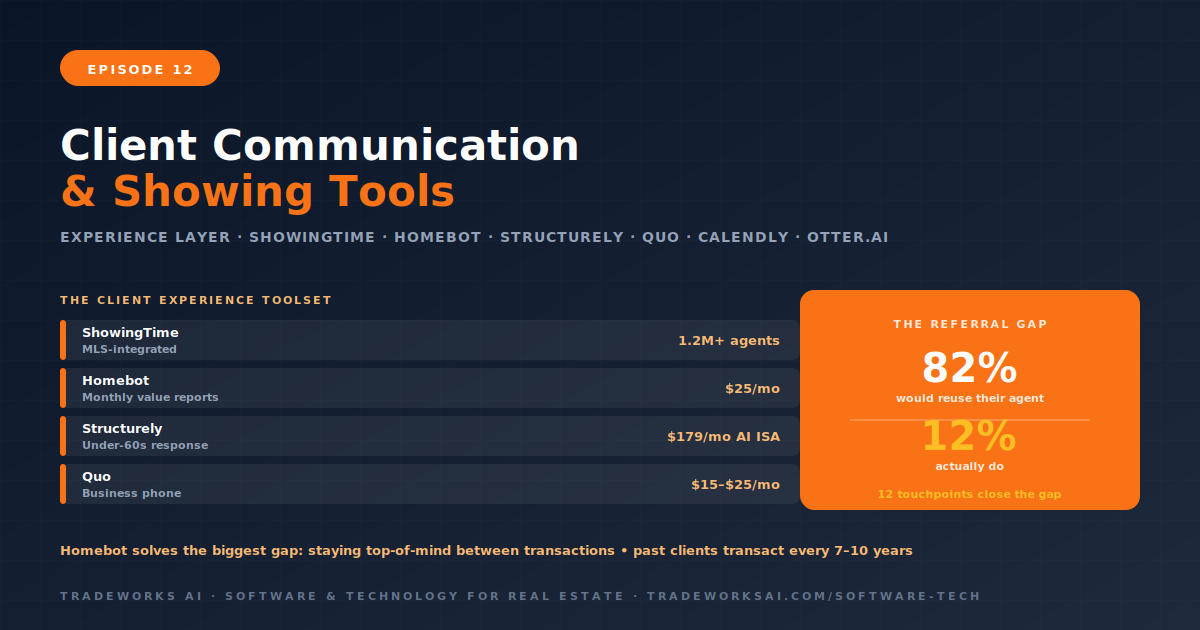

Client Communication and Showing Tools for Real Estate Agents: The Experience Layer That Wins Referrals

Continue the Real Estate Tech Stack series with Part 12 of 14.

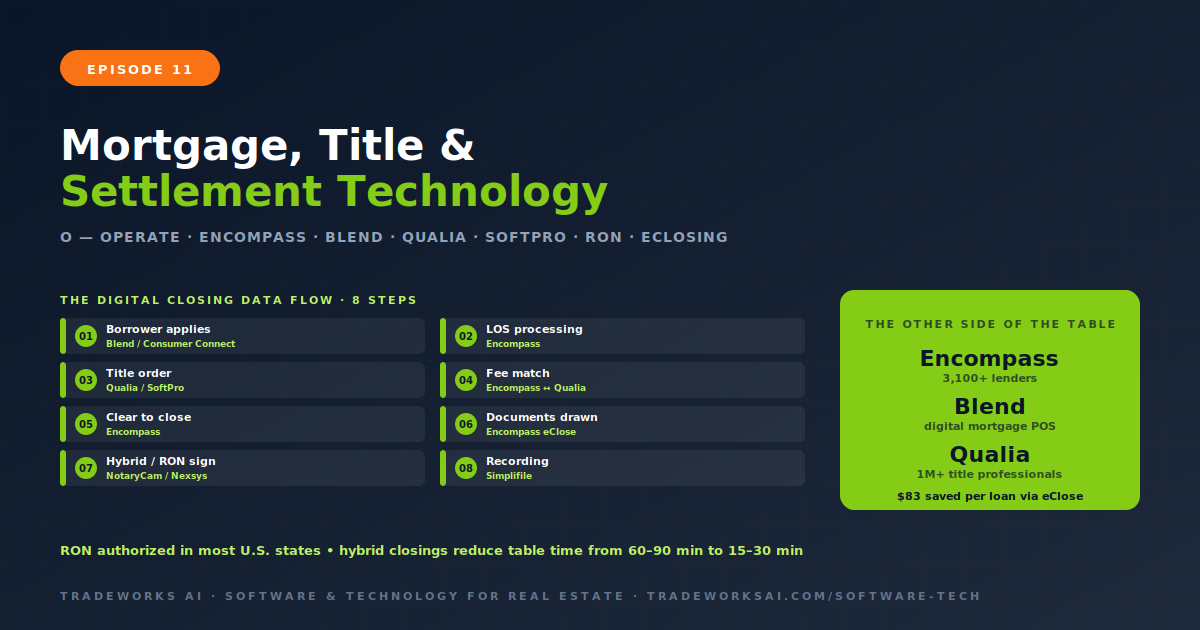

Most real estate agents never touch mortgage origination software or title production platforms directly. Encompass, Blend, Qualia, and SoftPro are tools used by their lending and title partners. But understanding how these systems work — and how they connect to the agent’s side of the transaction — makes the difference between an agent who passively waits for closing updates and one who proactively manages the transaction timeline, communicates intelligently with lenders and title companies, and delivers a client experience that feels seamless from contract to keys. In 2026, digital closings, Remote Online Notarization, and integrated lender-title workflows are transforming the closing process. This episode maps the technology landscape on the other side of the closing table and shows agents how to leverage that knowledge to close deals faster and with fewer surprises.

The agent does not originate the loan or produce the title commitment. But the agent is the client’s primary point of contact throughout the transaction and is often expected to explain what is happening, why it is delayed, and when it will be resolved. An agent who understands that their lender uses Encompass and their title company uses Qualia can ask informed questions: “What conditions are outstanding in Encompass?” instead of “When will we close?” The first question gets a specific answer. The second gets a vague one.

Understanding your partners’ technology also helps you choose better partners. A lender using Blend’s digital mortgage application delivers a faster, smoother borrower experience than one using a paper application faxed to processing. A title company on Qualia with eClosing capabilities offers digital signing and real-time status updates that a title company on legacy software cannot match. The technology your partners use directly impacts your client’s experience, your transaction timeline, and your reputation.

Encompass by ICE Mortgage Technology is the industry-standard loan origination system used by over 3,100 lenders and investors. It is the single system of record for the mortgage process: application intake, processing, underwriting, compliance, closing, and delivery to the secondary market. More loans are originated through Encompass than any other platform. For agents, this means your lender almost certainly uses Encompass or a competing LOS, and understanding the basic workflow helps you communicate more effectively.

The key concept for agents: a loan file in Encompass moves through defined stages, and at each stage, specific conditions must be satisfied before the file advances. When your lender says “we’re waiting on conditions,” they mean specific documents or verifications required by the underwriter before the loan can move to clear-to-close status. Asking “what specific conditions are outstanding?” gives you actionable information to relay to your client, coordinate document delivery, and prevent delays.

Encompass eClose is the digital closing module that enables lenders to draw closing documents, engage borrowers for e-signing, collaborate with settlement agents, and deliver closed loans to investors — all within the same system. Lenders using eClose report saving approximately $83 per loan by eliminating manual processes and reducing errors.

Blend is a digital lending platform that transforms the borrower’s mortgage application experience from a paper-heavy, multi-day process into an online, data-driven workflow that can be completed in minutes. The platform pre-fills application data by connecting to borrower financial accounts, employment databases, and asset sources. Borrowers can complete their application, upload documents, and track their loan status from their phone.

For agents, a lender partner who uses Blend means your buyer clients experience a faster, less frustrating application process. Pre-approvals come back faster. Document collection happens digitally. Status updates are available in real time. When you refer a buyer to a lender, asking whether they offer a digital application experience — and whether they use Blend or a comparable platform — is a legitimate quality-of-service question.

Beyond the LOS, modern mortgage technology includes point-of-sale platforms that provide the borrower-facing interface: online applications, document upload portals, loan status tracking, and digital pre-approval letters. Encompass Consumer Connect, Blend, and standalone POS platforms like Maxwell and SimpleNexus serve this function. The quality of the borrower’s digital experience is a direct reflection on the lender — and by extension, on the agent who recommended that lender.

Qualia is the leading cloud-based title, escrow, and closing platform, used by over one million title, escrow, mortgage, and real estate professionals. The platform replaces the fragmented workflows of legacy title production with a unified system: title search management, document preparation, settlement statement generation, escrow accounting, wire transfer management, and closing coordination — all in one platform. Users report a 75% reduction in workload after adoption.

For agents, Qualia’s Connect feature is the most relevant capability. Qualia Connect provides a secure portal where agents (and buyers, sellers, and lenders) can view real-time transaction status, access documents, and communicate with the title team without phone calls or email chains. Commitments, closing disclosures, settlement statements, and closing protection letters are automatically shared with the appropriate parties. If your title company uses Qualia, you have visibility into the closing process that agents working with legacy title companies do not.

SoftPro is another major title production platform, particularly popular in the eastern United States. RamQuest (now part of Black Knight) has a significant installed base, though some users are migrating to Qualia for its modern interface and cloud-native architecture. ResWare, now part of the Qualia ecosystem through Adeptive Software, serves enterprise title operations. For agents, the platform your title company uses matters less than whether that platform enables digital collaboration, real-time status updates, and eClosing capabilities.

Digital closings exist on a spectrum. A fully paper closing requires all parties to be physically present, signing every document with wet ink. A hybrid closing allows some documents to be signed electronically in advance, with only the deed, note, and notarized documents requiring ink signatures at the closing table. A full eClosing allows all documents to be signed electronically, with the notarization happening either in person (In-Person Electronic Notarization) or remotely via video (Remote Online Notarization).

In 2026, hybrid closings are becoming the norm for standard residential transactions. The borrower signs 80 to 90% of the closing package electronically before the closing appointment, leaving only the documents requiring notarization for the table. This reduces the time at the closing table from 60 to 90 minutes to 15 to 30 minutes. For agents and their clients, this is a dramatically better experience.

RON enables a notary to verify identity, witness signatures, and apply a notarial seal via a live audio-video connection. The signer does not need to be physically present with the notary. As of 2026, RON is authorized in the majority of US states, though acceptance varies by lender, title underwriter, and county recording office. RON is particularly valuable for relocation buyers, military personnel, investors purchasing remotely, and any party who cannot be physically present at closing.

Platforms like NotaryCam, Nexsys, and Qualia’s own RON capabilities power these remote closings. Encompass eClose and Simplifile enable the electronic recording of notarized documents at the county level, completing the fully digital closing chain from application to recording.

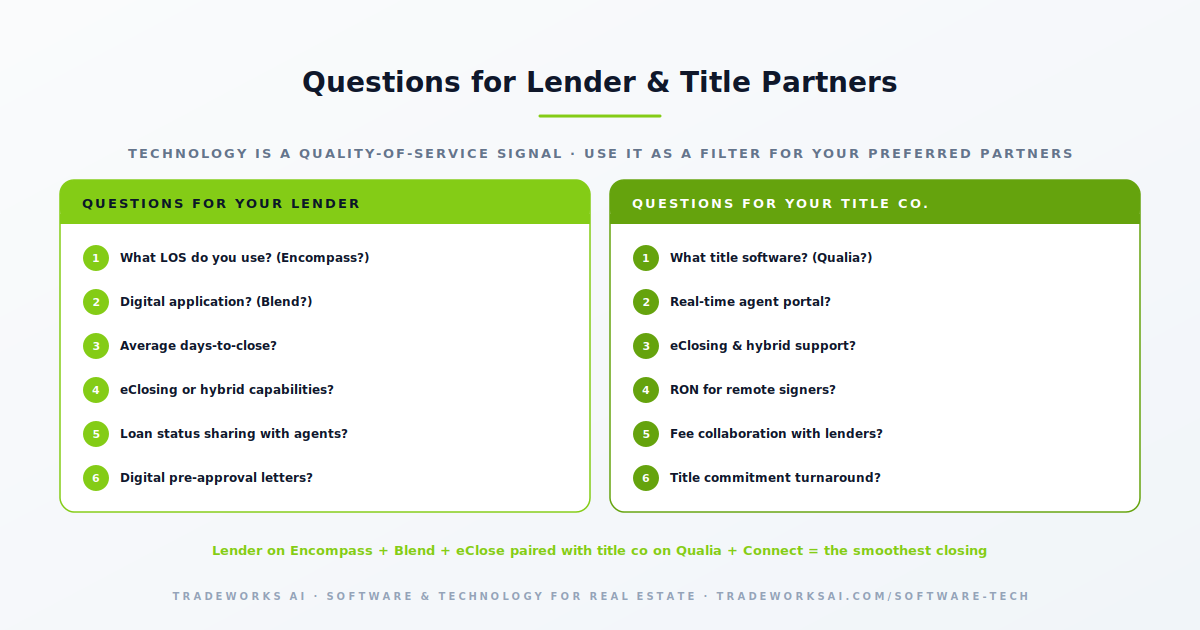

What loan origination system do you use? Do you offer a digital mortgage application (Blend, Consumer Connect, or comparable)? What is your average days-to-close? Do you offer eClosing or hybrid closing capabilities? How do you communicate loan status updates to agents — automated portal, email, or phone only? Can your system generate a digital pre-approval letter that my clients can share instantly?

What title production software do you use? Do you offer a real-time agent portal for transaction status (like Qualia Connect)? Do you support eClosing and hybrid closings? Do you offer RON for remote signers? How do you handle fee collaboration with lenders to prevent Closing Disclosure mismatches? What is your average turnaround time from title order to commitment delivery?

The agents who deliver the best client experience in 2026 are not just choosing lenders and title companies based on relationships and rates. They are choosing partners whose technology enables faster closings, better communication, and fewer surprises. A lender on Encompass with Blend for applications and eClose for digital closings, paired with a title company on Qualia with Connect and RON capabilities, creates a technology-integrated closing experience that reduces friction at every stage.

This does not mean you should only work with partners on these specific platforms. It means you should evaluate your partners’ technology capabilities as part of your selection criteria. The partner who offers you real-time status updates, digital document collaboration, and eClosing options is going to produce a better client experience than the partner who communicates by phone and sends documents by fax.

No. These are tools used by your lending and title partners. Agents benefit from understanding how they work so they can communicate more effectively with their partners, ask informed questions about loan and title status, and choose partners whose technology enables faster, smoother closings.

eClosing refers to any closing where some or all documents are signed electronically. A hybrid eClosing allows pre-signing of most documents with only notarized documents signed at the table. RON (Remote Online Notarization) specifically allows the notarization itself to happen remotely via video, enabling fully remote closings where no party needs to be physically present.

As of 2026, the majority of US states have enacted RON legislation. However, acceptance varies by lender, title underwriter, and county recording office. Agents should verify RON availability with their title company for each specific transaction. Even in states that authorize RON, not all lenders or investors accept RON-executed documents.

It enables you to ask specific questions (“what conditions are outstanding?” instead of “when will we close?”), choose partners whose technology delivers better client experiences, set accurate closing timeline expectations, and troubleshoot delays by understanding where in the digital workflow the file is stalled.

You should include technology capability as one factor in your lender recommendations alongside rates, responsiveness, product range, and reliability. A lender with a digital application, fast pre-approvals, and eClosing capabilities delivers a measurably better buyer experience. Disclosing your recommendation criteria to clients maintains transparency and trust.

Most agents buy tools in reaction to problems. The result: disconnected subscriptions that duplicate data and create more friction than they solve. The CLOSE Stack Self-Assessment grades your stack across all 5 layers and identifies the highest-leverage gap to close first.

Continue the Real Estate Tech Stack series with Part 12 of 14.

Continue the Real Estate Tech Stack series with Part 13 of 14.